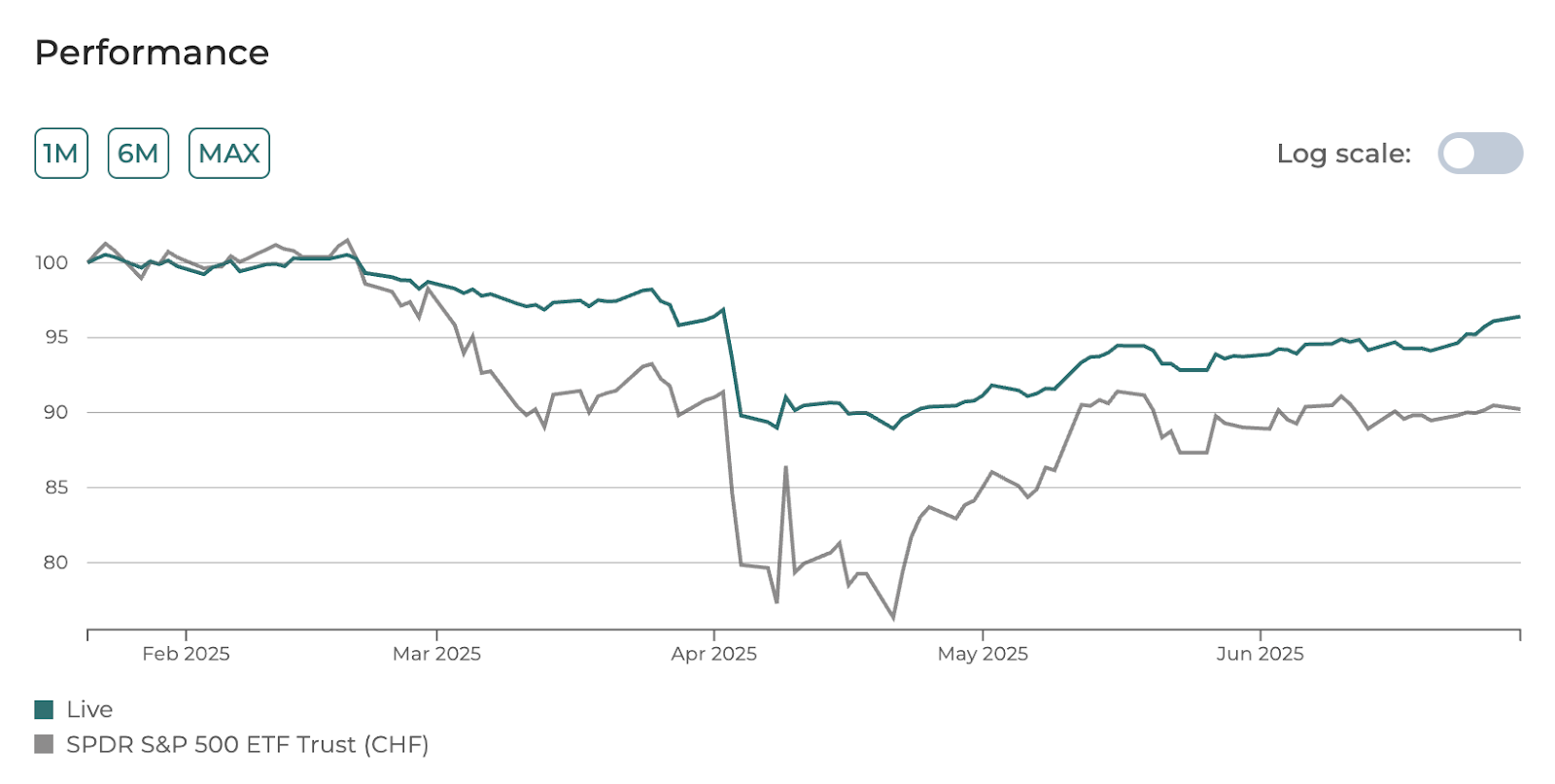

Over the past months, we’ve received questions from both clients and prospects regarding the recent performance of the Alquant Long/Short Equity CHF AMC, particularly around its role as an absolute return strategy.

The main concern relates to the drawdown experienced in April. While the strategy is designed to perform in a wide range of market conditions, certain unforeseen, one-off events, such as the Liberation Day tariffs’ announcement, can temporarily disrupt short-term performance. We have previously provided in-depth commentary on why our system is not built to anticipate such exogenous events. For more details, we encourage you to revisit our analysis: https://www.alquant.com/news-insights/aqls-review-navigating-an-extraordinary-market-event

Without this specific event, the strategy would have delivered a positive return in CHF year-to-date.

Another key consideration is the currency denomination of our strategy. Many absolute return or long/short equity hedge funds are denominated in USD and thus benefit from the elevated U.S. risk-free rate, which acts as a nominal performance tailwind. In contrast, our AMC is denominated in CHF, a currency with a significantly lower risk-free rate, which can result in a relative performance gap when compared to USD-based peers.

However, it's important to highlight that our strategy remains competitive when viewed on a currency-adjusted basis. When reconverted to CHF, or even when compared on a CHF-hedged basis (due to Cross Currency Basis), our approach maintains a strong edge. This is because we use futures contracts for market exposure while keeping the collateral in CHF, thereby preserving the integrity of the base currency and shielding investors from potential long-term depreciation of the USD.

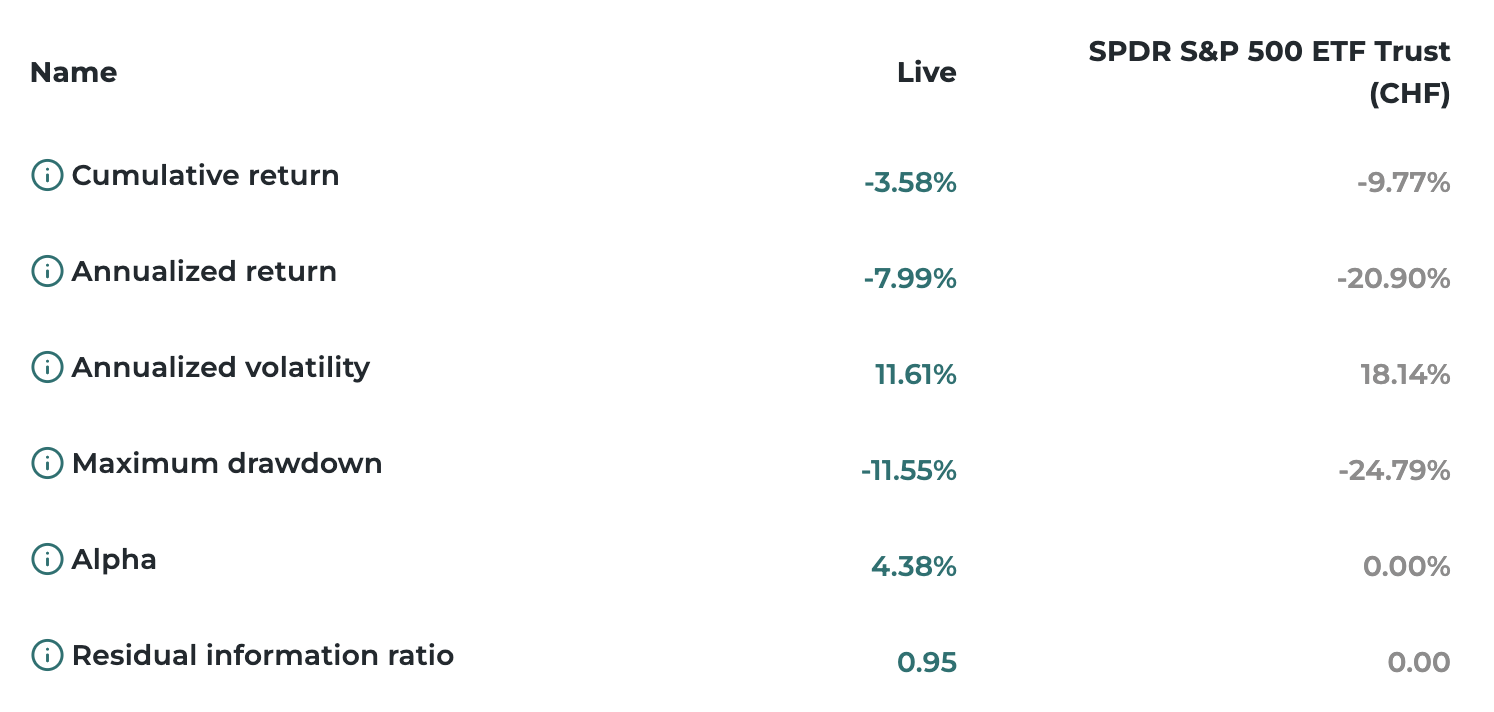

Despite these headwinds, the risk-adjusted metrics remain strong:

- Since inception, the Alquant Long/Short Equity CHF AMC has delivered a positive alpha and a high information ratio when measured against the S&P 500 in CHF.

- On an absolute basis, the AMC has even outperformed the S&P 500 in CHF since launch, validating the robustness of the underlying model.

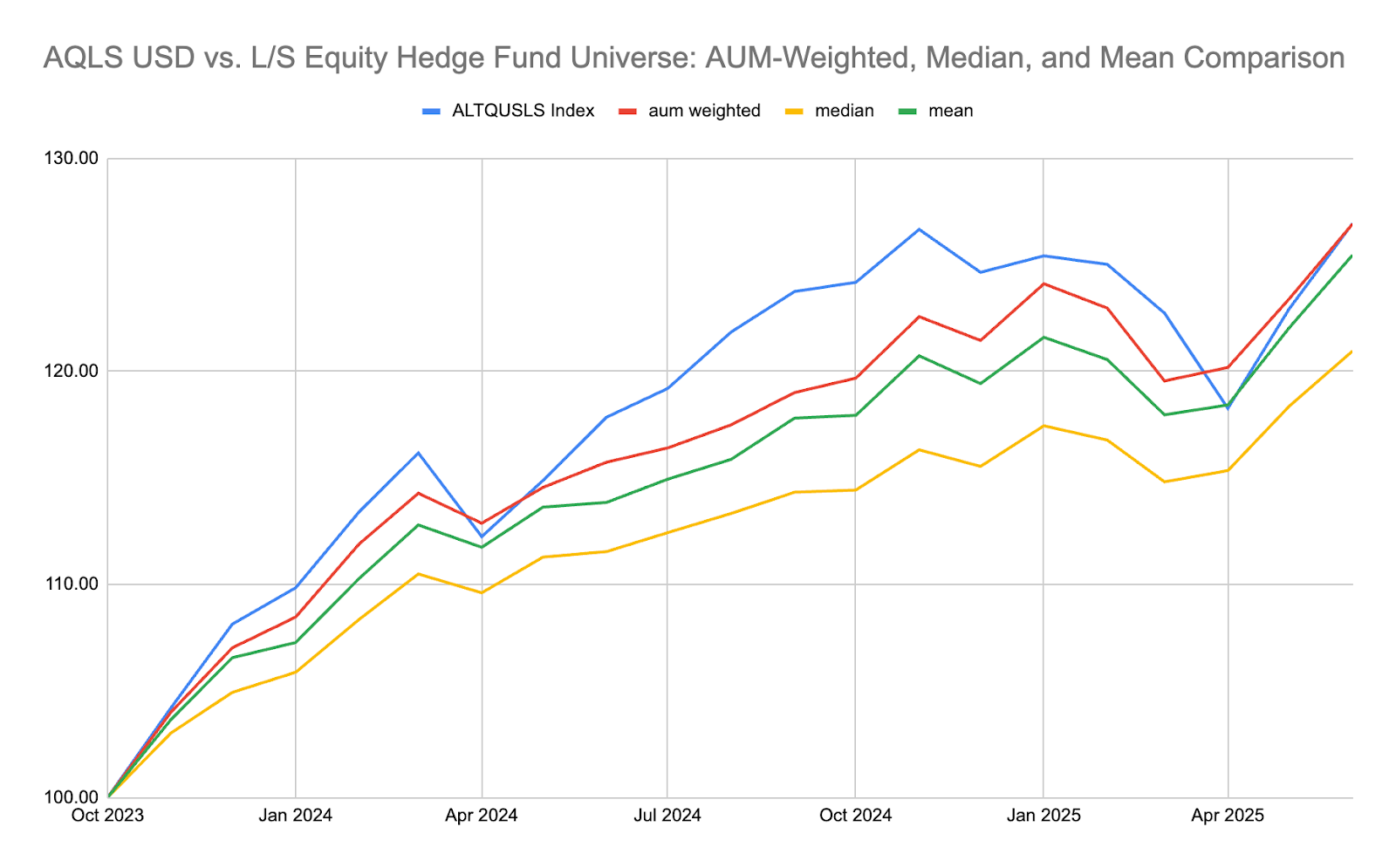

Furthermore, when comparing our Long/Short Equity strategy in USD to a peer group of over 1,000 Long/Short Equity hedge funds (based on AuM-weighted, median, and mean returns as of end-June), our performance stands very competitively. This is especially noteworthy considering our strategy offers daily, or even intraday, liquidity, while many competitors only provide quarterly redemptions.

We acknowledge the challenges faced in April, but we also take pride in the resilience shown in February and March, where our strategy slightly outperformed its benchmarks. We remain focused on long-term performance, risk management, and transparency.

Alquant, a Swiss Fintech and quantitative asset manager, is transforming asset management with innovative solutions. Leveraging deep financial and technological expertise, we offer a range of services including investment products, quantitative research, and software solutions, empowering financial institutions to create the financial products of the future.

© 2018-2024 Alquant SA. All Rights Reserved.

.svg)